Florida’s Personal Injury Protection under § 627.736 covers 80% of medical expenses and 60% of lost wages up to a $10,000 cap — but PIP does not cover pain and suffering, and the $10,000 limit rarely covers serious injuries from a Broward County car accident.

Mark T. Stern, Esq., is a personal injury attorney serving Pompano Beach from Lauderdale-By-The-Sea, Florida. Mark spent 12 years as a casualty claims adjuster for national insurance carriers and understands exactly how insurers process, delay, and underpay PIP claims.

Key Takeaways

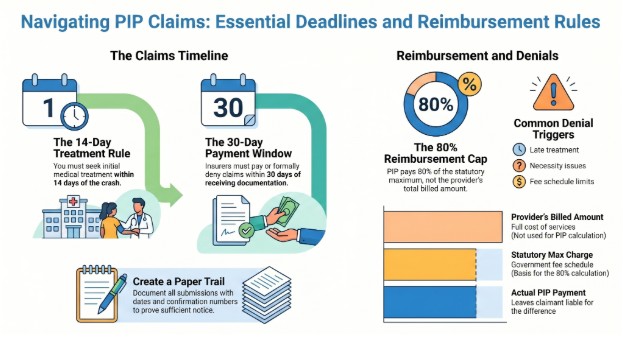

- PIP under § 627.736 requires initial medical treatment within 14 days of the crash, or benefits are eliminated entirely.

- The $10,000 PIP medical cap drops to $2,500 when a qualified provider determines no Emergency Medical Condition exists.

- Florida’s serious injury threshold under § 627.737 controls whether you can file a lawsuit against the at-fault driver for damages beyond PIP.

- Mark T. Stern operates on a contingency fee basis — no fee unless he recovers compensation.

What Does Florida PIP Insurance Cover Under § 627.736?

PIP covers 80% of reasonable and necessary medical expenses, 60% of lost wages, and a $5,000 death benefit — all subject to a $10,000 aggregate policy limit and strict eligibility conditions defined in Florida Statutes § 627.736. The policyholder’s own insurer pays these benefits regardless of who caused the accident.

| PIP Benefit | Coverage | Cap | Statute Subsection |

| Medical expenses | 80% of reasonable and necessary medical, surgical, dental, ambulance, and rehabilitative services | $10,000 (with EMC) or $2,500 (without EMC) | § 627.736(1)(a) |

| Lost wages (disability) | 60% of lost gross income | Included in the $10,000 aggregate | § 627.736(1)(b) |

| Death benefit | Lump sum payable to the surviving family | $5,000 | § 627.736(1)(c) |

| Replacement services | Reimbursement for household services that the injured person can no longer perform | Included in the $10,000 aggregate | § 627.736(1)(b) |

Who Qualifies for PIP Benefits

PIP extends to the named policyholder, relatives residing in the same household, passengers in the policyholder’s vehicle, and pedestrians or cyclists struck by the insured vehicle.

Each qualifying person uses the policyholder’s $10,000 PIP limit, so multiple injured parties in a single crash can exhaust the policy faster.

The Emergency Medical Condition Determination

A qualified medical provider must determine whether the injured person has an Emergency Medical Condition within the first 14 days of treatment.

An EMC — defined as a condition placing the patient’s health in serious jeopardy — unlocks the full $10,000 in medical benefits.

Without an EMC determination, medical benefits are capped at $2,500 under § 627.736(1)(a), and services from massage therapists and acupuncturists become ineligible for PIP reimbursement entirely.

Exhausted PIP benefits and denied medical claims leave Broward County accident victims paying out of pocket for injuries someone else caused. Mark T. Stern brings 12 years of insurance-industry experience to every PIP dispute. Schedule a free consultation today.

How Do You File a PIP Claim After a Car Accident in Broward County?

Report the accident to your own auto insurance carrier — not the at-fault driver’s insurer — within the timeframe specified in your policy, and seek initial medical treatment within 14 days of the crash under § 627.736(4)(c).

Your insurer processes PIP claims regardless of fault because Florida’s no-fault system routes initial medical and wage-loss costs through the policyholder’s own coverage.

The 30-Day Payment Deadline

Florida Statutes § 627.736(4)(b) requires your insurer to pay or formally deny a PIP claim within 30 days of receiving written notice of the covered loss and supporting documentation.

Benefits that remain unpaid for 30 days are considered overdue and may incur interest penalties. Documenting every submission with dates, confirmation numbers, and copies of medical records creates a paper trail that prevents the insurer from claiming insufficient notice.

Common PIP Claim Denials

Insurers deny PIP claims for three primary reasons: treatment initiated after the 14-day window, services deemed not medically necessary, and charges exceeding the fee schedule limits under § 627.736(5)(a).

The fee schedule provision allows insurers to cap reimbursement at 80% of the statutory maximum charge — not 80% of the provider’s billed amount.

This distinction frequently results in underpayment, leaving the injured person responsible for the difference between what the provider billed and what PIP actually paid.

What Is the Difference Between PIP Benefits and a Personal Injury Lawsuit?

PIP pays a fixed percentage of medical expenses and lost wages from your own policy regardless of fault, while a personal injury lawsuit seeks full compensation from the at-fault driver for economic and non-economic damages that PIP does not cover.

The two systems operate under different legal frameworks, funding sources, and damage categories.

| Category | PIP Benefits (§ 627.736) | Personal Injury Lawsuit |

| Who pays | Your own auto insurer | The at-fault driver’s insurer or the driver personally |

| Fault required | No — benefits paid regardless of fault | Yes — you must prove the other driver’s negligence |

| Medical expenses | 80% of reasonable costs, capped at $10,000 or $2,500 | 100% of past and future medical expenses |

| Lost wages | 60% of gross income, included in the $10,000 cap | 100% of lost wages and lost earning capacity |

| Pain and suffering | Not covered | Recoverable with no statutory cap in most car accident cases |

| Emotional distress | Not covered | Recoverable |

| Property damage | Not covered under PIP (covered by PDL) | Recoverable |

| Death benefit | $5,000 lump sum | Full wrongful death damages under § 768.21 |

| Filing threshold | None — file with your own insurer | Must meet serious injury threshold under § 627.737 |

PIP functions as a first layer of coverage designed to pay quickly. A personal injury lawsuit functions as the path to full compensation when injuries are serious enough to exceed what PIP was designed to cover.

When Can You Step Outside Florida’s No-Fault System to Sue the At-Fault Driver?

You can file a lawsuit against the at-fault driver when your injuries meet the serious injury threshold defined in Florida Statutes § 627.737: significant and permanent loss of an important bodily function, permanent injury within a reasonable degree of medical probability, or significant and permanent scarring or disfigurement.

Meeting any one of these three conditions removes the no-fault barrier.

Medical Documentation Controls the Threshold Determination

Treating physicians, orthopedists, neurologists, and independent medical examiners provide the records that establish whether injuries meet the statutory threshold.

Insurance companies challenge threshold determinations by commissioning their own IMEs and arguing that injuries are temporary, pre-existing, or unrelated to the accident.

Mark T. Stern spent 12 years reviewing exactly these IME reports from the insurer’s side — he knows which documentation forces the insurer to concede threshold and which gaps adjusters exploit to deny it.

Florida’s Modified Comparative Negligence Rule

Even after meeting the serious injury threshold, Florida Statutes § 768.81 — as amended by HB 837 in March 2023 — bars recovery entirely when a plaintiff is found 51% or more at fault. Compensation for plaintiffs at 50% fault or less is reduced proportionally by their fault percentage.

Adjusters routinely inflate the claimant’s share of fault to push the allocation past the 51% bar.

Threshold determinations denied and inflated fault allocations cost Broward County accident victims their right to full compensation. Mark T. Stern spent 12 years inside the insurance industry and recognizes those tactics immediately. Request your free case evaluation now.

What Happens When Your $10,000 PIP Coverage Runs Out?

The $10,000 PIP cap is frequently exhausted within the first weeks of treatment after a serious car accident on I-95 or Federal Highway. Emergency room visits, diagnostic imaging, and initial orthopedic consultations alone can consume the full $10,000 — leaving nothing for physical therapy, follow-up appointments, or ongoing rehabilitation.

Coverage Sources After PIP Exhaustion

Health insurance, MedPay (Medical Payments coverage), and uninsured/underinsured motorist coverage can absorb costs after PIP runs out, but none of these sources compensate for pain and suffering, emotional distress, or lost earning capacity.

Pursuing a lawsuit against the at-fault driver under § 627.737 becomes the only path to recovering non-economic damages and the remaining 20% of medical expenses and 40% of lost wages that PIP never covered.

The Two-Year Filing Deadline Still Applies

Florida’s statute of limitations under § 95.11 gives you two years from the crash date to file a personal injury lawsuit — regardless of whether your PIP claim is still open. Waiting for PIP to resolve before consulting an attorney risks missing the filing window entirely.

Insurance companies are aware of this deadline and routinely stretch PIP processing timelines, consuming months of the two-year window.

How Much Does It Cost to Hire an Attorney for a Florida PIP Dispute?

Mark T. Stern operates on a contingency fee basis for all personal injury and PIP dispute cases — the client pays no upfront retainer, no hourly fees, and no out-of-pocket costs during representation.

The firm collects a fee only when it recovers compensation through a settlement or court verdict.

Florida law requires all contingency fee agreements to be in writing and signed by both the attorney and the client. The attorney reviews the fee agreement in detail during the initial consultation so you understand the exact terms before representation begins.

The contingency fee structure eliminates the financial barrier that prevents many Broward County accident victims from challenging PIP denials or pursuing lawsuits against at-fault drivers.

Frequently Asked Questions

What does Florida PIP insurance cover after a car accident?

PIP under Florida Statutes § 627.736 covers 80% of reasonable medical expenses and 60% of lost wages, subject to a $10,000 aggregate cap. A $5,000 death benefit is also payable to surviving family members. PIP does not cover pain and suffering or property damage.

What happens if I do not see a doctor within 14 days of a Florida car accident?

Florida Statutes § 627.736(4)(c) eliminates PIP benefits entirely if initial medical treatment does not begin within 14 days of the crash date. The 14-day rule applies regardless of when symptoms appear, and no exception exists for delayed-onset injuries such as whiplash.

What is an Emergency Medical Condition under Florida PIP law?

An EMC under § 627.736(1)(a) is a condition placing the patient’s health in serious jeopardy. A qualified provider must determine EMC status to unlock the full $10,000 PIP medical benefit. Without an EMC determination, medical benefits are capped at $2,500 for the entire claim.

How long does my insurance company have to pay a Florida PIP claim?

Florida Statutes § 627.736(4)(b) requires insurers to pay or formally deny a PIP claim within 30 days of receiving written notice and supporting documentation. Benefits unpaid for 30 days or more are considered overdue and may incur interest penalties under the statute.

Can I sue the other driver if my PIP coverage runs out in Florida?

Only if your injuries meet the serious injury threshold under Florida Statutes § 627.737 — significant and permanent loss of an important bodily function, permanent injury within reasonable medical probability, or significant and permanent scarring or disfigurement. Exhausting PIP alone does not authorize a lawsuit.

Does PIP cover passengers and pedestrians in Florida?

PIP under § 627.736(1) extends to the named policyholder, relatives residing in the same household, passengers in the insured vehicle, and pedestrians or cyclists struck by the insured vehicle. Each qualifying person accesses the policyholder’s $10,000 policy limit.

What is the difference between PIP and bodily injury liability insurance in Florida?

PIP pays the policyholder’s own medical and wage-loss expenses regardless of fault. Bodily injury liability insurance pays the other driver’s damages when the policyholder is at fault. Florida requires PIP but does not require bodily injury liability coverage, leaving many at-fault drivers with no policy to cover their injuries.

Can my insurer pay less than 80% of my medical bills under PIP?

Florida Statutes § 627.736(5)(a) allows insurers to limit reimbursement to 80% of the statutory fee schedule maximum — not 80% of the provider’s billed amount. The provider may bill $200 for a service with a fee schedule maximum of $150, and the insurer pays $120 (80% of $150), not $160.

What happens if my PIP claim is denied in Florida?

Insurers deny PIP claims for treatment initiated after the 14-day window, services deemed not medically necessary, or charges exceeding the statutory fee schedule. An attorney can challenge the denial through a demand letter, and if the insurer does not resolve the dispute, through civil litigation under § 627.736.

Does hiring an attorney for a PIP dispute cost anything upfront?

Mark T. Stern operates on a contingency fee basis for all PIP disputes and personal injury cases. The client pays no retainer, no hourly fees, and no costs unless the firm recovers compensation. The fee percentage is agreed in writing before representation begins.

A $10,000 PIP cap and a 14-day treatment deadline mean most Broward County crash victims exhaust coverage before treatment ends. Mark T. Stern puts 12 years of insurance-side experience to work on every case. Contact the firm for a free consultation.